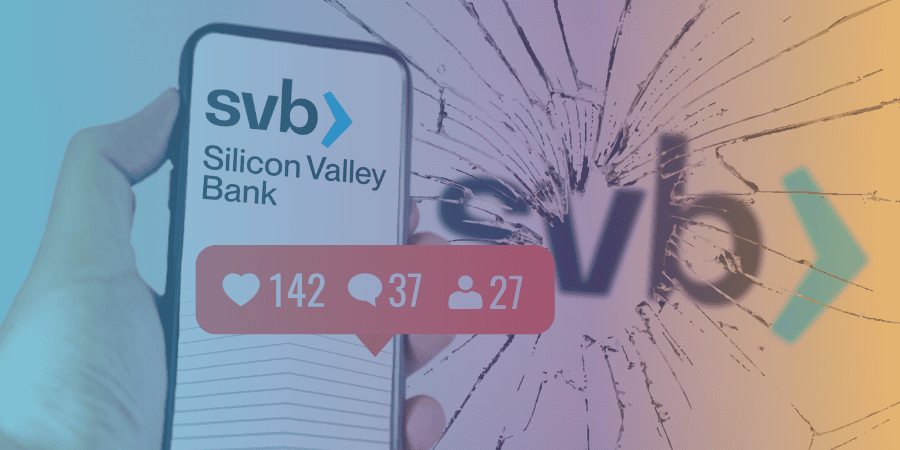

Silicon Valley Bank (SVB) experienced a rapid collapse, leaving experts questioning the role social media played in the crisis.

The speed of the bank’s decline has led to plummeting shares in banks worldwide, heightening fears of a wider financial crisis.

Bank executives and regulators have been forced to move quickly in response to the unprecedented situation.

The collapse of SVB has had far-reaching effects on its core consumer base, the tech industry of the San Francisco Bay Area.

US authorities guaranteed all deposits in SVB and smaller bank Signature within 48 hours of the collapse, and the Swiss central bank provided Credit Suisse with a $54bn loan after its share price plunged.

SVB’s collapse was the second-largest bank failure in US history, and the first-ever “Twitter-fuelled bank run.”

The bank’s troubles began when the Federal Reserve raised interest rates rapidly, resulting in the devaluation of bonds owned by SVB.

Many of its customers were also affected by interest rate rises and needed to access their deposits for day-to-day business expenses.

With the bank’s investments losing value, it struggled to meet these demands.

Social Media Spreads Panic, Accelerating the Crisis

A decision to raise funds through a sale of shares led to the withdrawal of $40bn (one-fifth of SVB’s deposits) within just a few hours.

High-profile entrepreneurs and investors, such as Mark Tluszcz and Bill Ackman, used Twitter to sound the alarm, urging customers to withdraw their money.

The panic spread rapidly through social media, and experts believe that the ease of online banking access and the viral nature of social media played a significant role in the crisis.

Messages shared on social media platforms like Twitter and WhatsApp by influential figures in the tech and finance industries contributed to the frenzy.

As a result, many customers rushed to withdraw their funds, fearing the loss of their savings.

Michael Imerman, a professor at the Paul Merage School of Business at the University of California-Irvine, described the event as “a bank sprint, not a bank run,” with social media playing a central role.

Impact on the Tech Industry and the San Francisco Bay Area

The collapse of SVB has had far-reaching effects on its core consumer base, the tech industry of the San Francisco Bay Area.

Since its founding in 1983, the bank had been a key institution for venture capital firms and wealthy individuals in the tech world.

As the bank held $209bn in assets and $175bn in deposits, its failure has led to significant consequences for the tech industry and the local economy.

Federal Intervention and Criticism

The US authorities guaranteed all deposits in SVB and smaller bank Signature 48 hours after the collapse.

This federal intervention has been criticized for giving undue support to an institution that serviced the wealthy and higher-risk business ventures.

Steven Kelly at Yale’s program on financial stability argues that this intervention could set a precedent that allows other banks to engage in risky behavior, believing that the Fed will step in if things go awry.

However, it is not a full bailout, as those who invested in SVB stock will not be made whole.

Congressional Democrats Return SVB-Linked Donations

Top Democrats in Congress, including Senate Majority Leader Chuck Schumer and Representative Maxine Waters, have vowed to return campaign contributions tied to SVB.

Between 2017 and 2022, the bank donated over $50,000 to Republicans and Democrats on finance-related committees.

The returned donations will be sent to New York-based charities, as announced by Schumer’s office.

Banks and Regulators Grapple with Social Media’s Role in Financial Crises

The rapid collapse of SVB has forced regulators, policymakers, and bankers to examine the role social media played in the current upheaval and determine how they can adapt to the challenges it presents.

The unprecedented speed at which the crisis unfolded highlights the potential for social media to amplify panic and destabilize financial institutions.

As information and rumors can now spread faster than ever before, the ability of regulators and banks to respond effectively is being tested.

Need for Improved Communication and Crisis Management

In light of the role social media played in SVB’s collapse, there is a growing need for financial institutions and regulators to improve their communication strategies and crisis management plans.

This includes monitoring social media platforms to identify and address misinformation promptly and implementing measures to minimize the impact of potential bank runs.

Educating the Public and Promoting Financial Literacy

One possible solution to mitigate the risks associated with social media-fuelled financial crises is to educate the public on the importance of financial literacy.

By helping consumers understand the workings of the financial sector and the potential consequences of their actions, they may be less likely to react impulsively to online rumors and misinformation.

This could contribute to a more stable financial environment and reduce the risk of similar events in the future.

Regulation of Social Media and Financial Institutions

In response to the SVB crisis, some experts are calling for increased regulation of social media platforms and financial institutions.

This could involve implementing guidelines on the dissemination of financial information, preventing the spread of misleading or false news, and holding those who share such content accountable.

Additionally, increased oversight of financial institutions and their communication strategies may help prevent the rapid spread of panic and ensure that accurate information is being shared with the public.

Article In a Snapshot

- The rapid collapse of Silicon Valley Bank (SVB) has led to a reevaluation of the role social media plays in financial crises, as it amplified panic and destabilized the institution.

- Improved communication strategies and crisis management plans are necessary for financial institutions and regulators in light of social media’s role in the crisis.

- Educating the public on financial literacy and promoting responsible social media use can help mitigate the risks associated with social media-fueled financial crises.

- Some experts are calling for increased regulation of social media platforms and financial institutions to prevent the spread of misleading information and ensure accurate communication with the public.

- The SVB crisis highlights the need for regulators, policymakers, and banks to adapt to the challenges presented by the modern digital landscape.